On this page

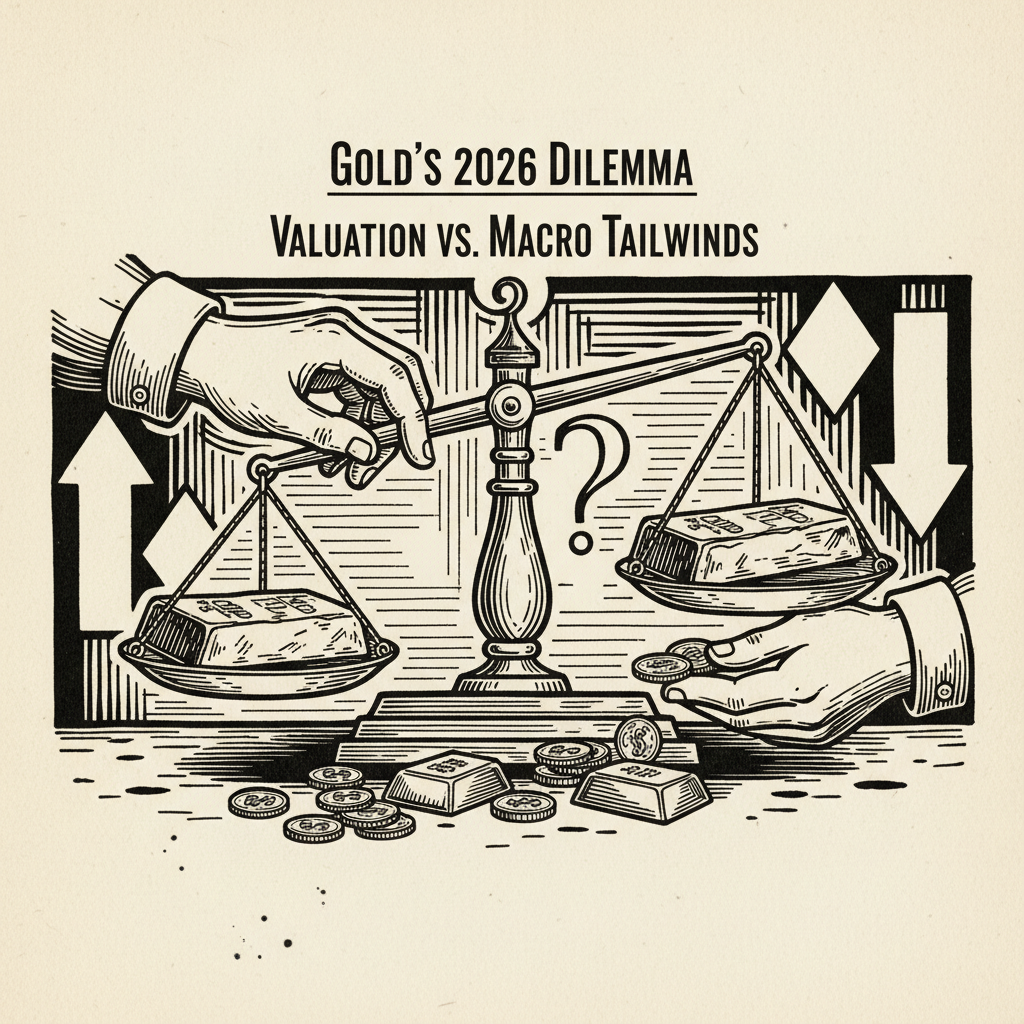

Gold’s 2026 dilemma: valuation vs. macro tailwinds

Gold faces a critical juncture where elevated prices collide with persistent monetary uncertainty, forcing investors to weigh stretched valuations against enduring structural support.

What to know

-

Gold has climbed over 27% from its October 2023 lows, raising questions about entry points at current levels

-

Central bank demand remains structurally robust despite price appreciation, with emerging market purchases continuing

-

The metal’s traditional inverse correlation with real yields has weakened, complicating traditional valuation frameworks

What’s changed in gold’s risk-reward equation?

The gold price trajectory since late 2023 has fundamentally altered the investment calculus. The metal rallied from around $1,820 per ounce in October 2023 to levels testing previous all-time highs - a 27%+ advance that occurred even as real yields remained elevated by historical standards.

The challenge facing investors now isn’t whether gold serves a portfolio purpose, but whether current valuations offer adequate compensation for the risks. At these levels, the margin of safety that existed 15 months ago has compressed considerably. Yet dismissing precious metals purely on price would ignore the structural shifts reshaping demand patterns.

Why does central bank buying still matter?

Central bank accumulation continues to provide a floor under prices that didn’t exist in previous cycles. Emerging market monetary authorities have been net buyers for 14 consecutive years, but the pace accelerated dramatically post-2022. This isn’t speculative positioning - it’s strategic reserve diversification with multi-year horizons.

This support matters because of its price-insensitivity. Unlike momentum-driven investors who chase performance, central banks appear willing to accumulate regardless of short-term valuations. This creates a persistent bid that absorbs supply shocks and dampens downside volatility, even if it doesn’t necessarily justify current multiples.

What are the broader market implications?

Gold’s resilience amid tightening monetary conditions appears to reflect something deeper about investor psychology. The traditional playbook - rising rates kill gold - has been disrupted. Markets are showing simultaneous strength in equities, elevated yields, and firm precious metal prices, a combination historically rare outside crisis periods.

This pattern suggests markets are pricing in tail risks that don’t yet appear in volatility indices. Whether it’s fiscal sustainability concerns, geopolitical fragmentation, or doubt about central banks’ inflation-fighting credibility, gold is behaving as if uncertainty itself has become structural rather than cyclical. That backdrop supports ongoing allocation even at rich valuations, though it doesn’t eliminate downside risk if those concerns prove overblown.

The recent headwinds facing gold’s record rally demonstrate that no trend moves in a straight line, particularly after such extended gains.

What historical patterns are relevant?

Previous gold peaks in 1980 and 2011 both ended badly for late-cycle buyers. Each followed extended rallies driven by macro fears that eventually subsided. The 1980 peak took 28 years to reclaim; 2011’s high wasn’t exceeded until 2020. Those cautionary episodes remind us that even assets with long-term merit can deliver punishing short-term results when purchased at extremes.

Yet current conditions differ in key respects. The 1980s saw aggressive monetary tightening that broke inflation psychology. The 2011-2015 period featured a strong dollar and collapsing commodity complex. Today’s environment shows neither decisive inflation victory nor broad commodity weakness.

What comes next depends on real yields and currency moves

Real yield direction remains the critical variable. If 10-year TIPS yields push sustainably above 2.5%, gold’s opportunity cost becomes harder to justify at current prices. Any pivot toward easier policy - whether forced by growth concerns or fiscal stress - could validate today’s valuations quickly.

The dollar’s trajectory against emerging market currencies also matters. Central bank buying accelerates when local currency depreciation makes dollar-denominated gold relatively cheaper for reserve managers. A stronger yuan or rupee could reduce that structural bid. This article is for informational purposes only and does not constitute financial advice. Always do your own research before making investment decisions.